Timeless Wisdom from Warren Buffett's Latest Letter

Warren Buffett’s annual letter to Berkshire Hathaway shareholders continues to be one of the most anticipated pieces of financial commentary each year. With more than seven decades of investing experience, Buffett’s insights go beyond market timing or short-term predictions. They offer foundational guidance—especially valuable in today’s uncertain environment.

Below are three enduring takeaways from the “Oracle of Omaha” and why they still matter for investors today.

1. Equities Are a Long-Term Inflation Hedge

“Paper money can see its value evaporate if fiscal folly prevails…Fixed-coupon bonds provide no protection against runaway currency…I have had to rely on equities throughout my life. In effect, I have depended on the success of American businesses, and I will continue to do so.” - Warren Buffet

Buffett emphasizes that equities remain his preferred investment vehicle because of their unmatched ability to outpace inflation over time—a point he highlights to counter media speculation around Berkshire Hathaway’s sizable cash holdings. While some interpreted the cash position as a signal of pessimism, Buffett clarifies that the vast majority of Berkshire’s assets remain in equities, reinforcing his long-term confidence in American businesses. For investors, the key takeaway is that staying on the sidelines poses its own risks—particularly the erosion of purchasing power in a high-inflation environment.

Figure 1: Growth of $1 (1927–2024)

Figure 1 which shows the growth of $1 from 1927 to 2024, visually underscores this point, illustrating how U.S. stocks have significantly outperformed both cash and inflation over the long term.Source: Avantis

2. True Value Lies in Quality at a Good Price

“We simply looked at their financial records and were amazed at the low prices of their stocks.”- Warren Buffet

Early in his career, Warren Buffett was a strict disciple of Benjamin Graham’s deep-value approach—seeking out companies trading below their book value, regardless of business quality. But as time went on, and with the influence of Charlie Munger, Buffett’s strategy evolved. He began favoring “wonderful companies at fair prices,” placing greater emphasis on profitability and overall business quality. This shift highlights an important lesson for investors: value isn’t just about buying cheap—it’s about buying wisely.

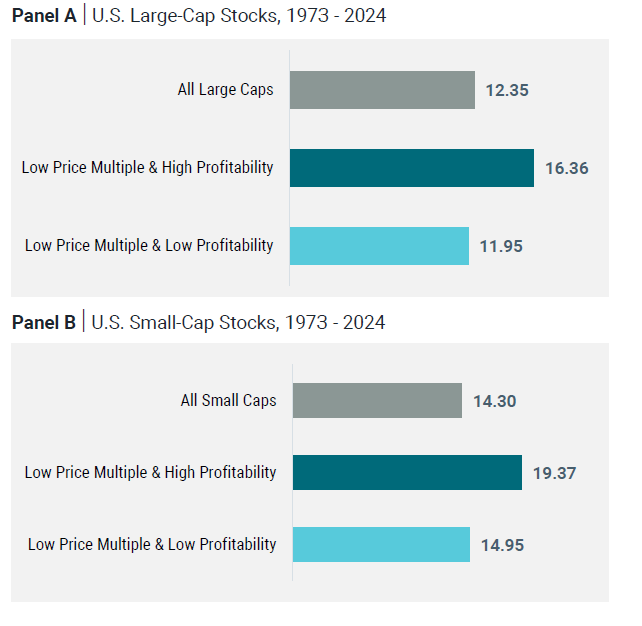

Figure 2: Value Is Found in Quality Companies with Good Prices

Figure 2 brings this concept to life by comparing the performance of low-priced stocks with varying levels of profitability. The results make it clear: companies with strong fundamentals and solid profits tend to outperform their lower-quality peers, even when both are priced attractively. Source: Avantis

3. Reinvestment and The Power Compounding

“Berkshire shareholders have participated in the American miracle by foregoing dividends, thereby electing to reinvest rather than consume. Originally, this reinvestment was tiny, almost meaningless, but over time, it mushroomed, reflecting the mixture of a sustained culture of savings, combined with the magic of long-term compounding.” Warren Buffet

Under Warren Buffett’s leadership, Berkshire Hathaway has paid just one dividend in over six decades—a decision that reflects his strong belief in the power of reinvestment and compounding over time. Buffett argues that reinvesting profits back into the business can generate far greater long-term value than distributing earnings to shareholders. This philosophy isn’t unique to Berkshire; other top-performing companies like Amazon and Tesla also choose to reinvest rather than pay dividends. For investors, the takeaway is clear: a high dividend yield isn’t always a mark of quality or strong returns.

Figure 3: Dividend Yield of the Top 10 Largest U.S. Companies

Figure 3 illustrates this point by showing that many of the largest and most successful U.S. companies pay little to no dividends, challenging the assumption that income payouts are the best indicator of investment strength. Instead, evaluating a company’s overall fundamentals—like growth potential and profitability—can offer a more complete picture.Source: Avantis Investors

Embrace Simplicity, Stay the Course. Buffett’s letter also reflects a humility that’s rare among business leaders. He candidly discusses mistakes and emphasizes transparency—reminding us that no investor is perfect. The key is to remain disciplined, focus on what you can control, and let time do the heavy lifting.

For long-term investors, Buffett’s words remain as powerful as ever: stick with quality, think long term, and trust in the power of compounding.